Quick Note: Papa Johns Takeout Order

Apollo PZZA takeout considerations for those looking for a slice of the action

Earlier today on June 11, 2025, Reuters reported that Apollo and Irth Capital Management had approached PZZA 0.00%↑ for a potential takeout at about ~$60 per share.

If we use the framework discussed in the below case study, we can quickly sketch out potential upside from current prices at ~$51.

Case Study: Art of the Deal

This post is the latest in a series of educational case studies designed to provide valuable insights for both retail investors and professional analysts.

In the above AEL case study, management had specific hurdles they needed to reach in order to see a payout. Thankfully, we have something similar at Papa John’s.

On July 19, 2024, the PZZA 0.00%↑ board granted one-time retention PRSU awards to management, including the interim CEO. Key characteristics of the award include:

Stock price hurdles at $65, $75, and $85

3-year performance period

Vesting on 4 year service period

Double trigger change in control provisions

The shares never quite reached the first hurdle, with a high of around ~$60 post-grant.

There are some unique dynamics here worth thinking through for the management. Timing is going to be very important with regards to how the grant hurdles trigger.

Game Planning

One of the big differences from the AEL grant is this:

If an executive’s employment is terminated by the Company without “Cause” (as defined the award agreement for the Retention Awards) before the Retention Awards have vested, the Retention Awards will vest based upon the actual achievement of the stock price hurdles through the date of the termination.

However, if the termination without Cause occurs within the first 18 months of the performance period and no stock price hurdles have been achieved by such date, 20% of the shares subject to the Retention Award will vest.

In addition, the award agreement for the Retention Awards provides for “double trigger” equity acceleration in the event that an executive is terminated in an “Involuntary Termination” (as defined in the award agreement) within twelve months following a “Corporate Transaction” (as defined in the Company’s 2018 Omnibus Incentive Plan).

There is a 20% downside floor upon a termination without cause within 18 months of the performance period.

This is actually a strong sign that they could have been fishing for a buyout within 18 months, insofar as there would be no way for the specific management personnel to be terminated without a CiC.

This is confirmed by the end of the exhibit discussing the performance grant:

Corporate Transaction

Notwithstanding anything herein to the contrary, the Performance Period shall end as of the effective date of a Corporate Transaction occurring on or prior to the third anniversary of the Grant Date.

In such event, the number of Restricted Stock Units that shall become Earned RSUs will be determined by the greatest of (a) 20% of the Target number of Restricted Stock Units subject to this Agreement, (b) the number of Earned RSUs achieved through the date of the Corporate Transaction based on attainment of the Share Price Hurdles prior to such date, or (c) the number of Earned RSUs that would be considered achieved based on the application of the per-Share transaction price in the Corporate Transaction to the Share Price Hurdles as determined by the Committee.

Subject to your continued Service through the first anniversary of a Corporate Transaction, you shall become fully vested in the number of Earned RSUs determined pursuant to the immediately preceding sentence.

So, in the event of a Change in Control, management has a 20% floor.

18 months from grant date is around January 2026, so management has about a 6 month timer before the only options for vesting the grant become:

Takeout for 20%+ vesting

Hit the price hurdles AND serve four years for full vesting

It would be so much easier for the team if they managed to get a $65 or $75 bid from any prospective suitor.

That’s a 27% upside from current prices at $51.

Big Buts

However, I am less inclined to believe that a transaction will occur compared to the AEL scenario for several reasons:

The grants were given to management before the current CEO joined. The current CEO doesn’t have this torque in his compensation package outside of RSUs and PSUs based on operating metrics with a TSR modifier.

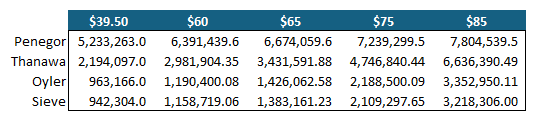

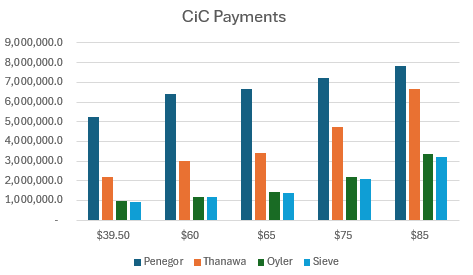

These CiC outcomes were generated with a $39.54 stock price, which was the price at the end of 2024.

Here’s the estimated payout for each of the officers at the different price levels. Because of the additional units unlocked by reaching higher price hurdles, the value of each incremental dollar between hurdles is higher (assuming they reach the next hurdle). For example, in the case of CFO Thanawala, the value of every dollar move between $60 and $65 is $59k, while the value of every dollar between $65 and $75 is $100k.

I ran the exercise just to make sure that there isn’t some obvious local minima that management would theoretically settle for.

In other words, there’s always a reason to try and get the higher price. That said, this exercise doesn’t discount for the four year service period requirement. If next quarter’s earnings are shaping up to be good, there’s an incentive to start soliciting new bids after the quarter ends to try and take advantage of the expected earnings pop AND to get the payout ahead of the service period. Remember that most of Q2 (ends 6/30) is already in hand.

These are all elements to consider if you’re looking at the name.

Paid subscribers, recall the rule of thumb for turnaround situations that I mentioned in the GRPN case study. It worked out very well for PZZA:

Keep reading with a 7-day free trial

Subscribe to Tarot Capital to keep reading this post and get 7 days of free access to the full post archives.