Case Study: Coupon Comeback

Groupon's 8x Return Since March 2023

On March 30 2023, Groupon GRPN 0.00%↑ appointed Dusan Senkypl—co-founder of Pale Fire Capital, its largest shareholder with roughly 22 percent of the stock—as interim chief executive officer and awarded him an unusually aggressive, high-risk pay package. Senkypl had joined Groupon’s board only nine months earlier, in June 2022.

CEO Senkypl’s compensation had an atypically low salary and incredible upside torque:

Mr. Senkypl, who will be based in the Czech Republic, will serve as Interim CEO for a term of one year pursuant to the Employment Agreement or until the Board appoints a permanent successor.

…

In connection with his appointment as Interim Chief Executive Officer, Mr. Senkypl will receive an annual base salary of approximately $19,000 and on March 30, 2023 (the “Grant Date”) he received a grant of 3,500,000 nonqualified stock options to purchase the Company’s common stock at a per share exercise price of $6.00 (“Options”) under the Groupon, Inc. 2011 Incentive Plan, as amended (the "Plan").

The Options will expire 3 years from the Grant Date, and will vest 1/2 on the date that is 1 year from the Grant Date and quarterly thereafter in four substantially equal installments, beginning on the date that is 1 year and 3 months from the Grant Date, or if the requisite approval of the Plan Amendment is received, will vest quarterly in eight substantially equal installments, beginning on the date that is 3 months from the Grant Date.

This was noteworthy for several reasons:

1 year employment agreement

High strike on the options vs. grant date value

Significant % of compensation to options and very little to cash

Half vesting in 1 year

At the time, the stock was trading at $3.50. The following day, shares gapped up to $4. Over the next month and a half, shares continued to decline to a low of $2.89 on 5/16/2023.

Just over two years later, shares achieved a price of $32.53 on 6/4/25, making for a 6-9x over the time period.

Fundamental Turnaround

Billings and gross/operating profits started to turn around in 2023, right around when the CEO compensation grant hit.

This suggests a question of causality. Did the CEO really make all those changes? Or was that always destined to happen and the CEO just got lucky?

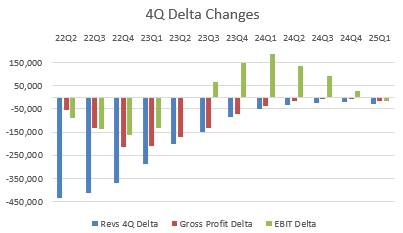

The below chart shows that revenues declined—and continued to decline—while operating income flipped from negative to positive. That suggests at least some competence on the management side in terms of taking out unneeded costs from SG&A.

Let me explain what ‘4Q Delta’ means. I take the nominal value of the past four quarters and subtract it by the prior four quarters. This gives me a number that represents the change in nominal value over that time period. If plotted on a bar chart, it gives a strong visual sense of trending direction. Functionally, it’s the same thing as a year over year comparison, but this smooths it out. Shoutout to

for showing me this little trick years ago.There were also a number of financing changes that reduced the going concern issues for the business. In early 2024, the company improved its liquidity by ~$100m through a combination of asset sales and a rights offering. In late 2024, about $200m in convertible debt was issued.

Ultimately, balance sheet judo and cost cutting are necessary, but not sufficient. The fundamentals and the end-markets need to turn around.

The pace of billings also seems to keep pace with the change in the stock price. Worth digging in here to tease out some of the factors involved.

25Q1 results prompted a massive move upwards in the stock price. Fundamentally the metric to track is North American billings. This gives insight into the biggest % of earnings and revenues. For example, in 25Q1, NA local gross profit was ~79% of all gross profit between all geographies and segments.

You can see that local gross billings stabilized, and even accelerated on the top-line as of 25Q1. This was and is likely the key metric to track for GRPN.

Of course, technical factors can contribute to sharp movements in stock price as well. I won’t pretend to know the ins and outs of technical dynamics—there more than enough peddlers of such wares on Twitter—but it’s worth paying attention to as an additional source of conviction. Short covering, in particular, can accelerate upwards moves.

It’s probably fair to assume that short covering contributed to some of the sharp moves year to date, though the recent spike in levels may also be a consequence of some convertible bond arbitrage.

More Aggressive Compensation

On May 7, 2024, CEO Senkypl was appointed as permanent CEO. Shares were trading around $11 at the time.

His pay package was still quite aggressive, but not as high-risk as the initial grant.

In connection with his appointment as CEO, Mr. Senkypl will receive (i) an annual base salary of $150,000 USD (which will be converted to his local currency of CZK at time of payment); (ii) a target bonus opportunity of up to a maximum of 150% of his base salary; and (iii) on May 1, 2024 (the “Award Date”), an award of 1,393,948 performance share units (“PSUs”) under that certain PSU Award Agreement (the “CEO PSU Award Agreement”) dated May 7, 2024, by and between Mr. Senkypl and the Company (the “CEO PSU Award”) and pursuant to the Groupon, Inc. 2011 Incentive Plan, as amended (the “Plan”).

…

The PSUs can only be earned if certain stock price hurdles ($14.86, $20.14, $31.01, and $68.82) are met during a performance period and Mr. Senkypl satisfies certain service conditions.

•Achievement of each stock price hurdle would entitle Mr. Senkypl to 25% of the target number of PSUs, subject to the service condition being met.

•The performance period begins on the Award Date and ends on the third anniversary of the Award Date. The stock price hurdles must be achieved during the measurement period. The measurement period for determination of any stock price hurdle achievement begins nine months from the Award Date.

While the base salary was dramatically increased against its prior state. The aggressive stock price hurdles should have indicated that the board—a controlled one—believed that there was more value to unlock.

I think there’s a reasonable conclusion that this grant was actually somewhat of a ‘dark arts’ grant, given that earnings happened a few days after and the stock price went up ~70% over the next week. Keep in mind that the grant was issued with full knowledge of 24Q1 earnings.

Of course, they don’t vest immediately, but these aren’t the sort of grants you give out in anticipation of underperformance.

Conclusion

GRPN is a very good example of an ideal incentive-driven setup. The grant should indicate the possibility of a turnaround, and traditional fundamental work follows from that insight.

We’ve seen a number of these turnaround grant stories and we’ve developed a a key rule of thumb to try and reduce drawdowns when trying to catch a knife. It’s very relevant to my post on JACK 0.00%↑.

Jack on Track

I like easy stocks—the ones that go up steadily with low volatility. This isn’t that. is the other kind. The gross kind. The one where even if you nail it, it’s not worth the emotional turmoil, and if you fail, you were a fool for even trying.

Key Rule of Thumb

It’s a very simple rule, and one that has worked on a number of Tarot Turnaround Trades:

Keep reading with a 7-day free trial

Subscribe to Tarot Capital to keep reading this post and get 7 days of free access to the full post archives.