Forfeiting $4M to Make $14M

Loan sharks turn misses into milestones with galaxy-brained accounting shenanigans

World Acceptance Corporation (WRLD 0.00%↑) is an $800m market-cap installment loan business that operates across 16 states in the southern and midwestern regions of the US. You don’t expect a modern day usury company to act in the most ethical fashion possible, and this management team doesn’t disappoint.

This write-up is structured into three parts:

Usury Company Behave Ethically Challenge (IMPOSSIBLE)

Brief Fundamental Overview

What’s Next?

Usury Company Behave Ethically Challenge (IMPOSSIBLE)

On October 15, 2018, with shares trading around $100, the Board of WRLD approved a new long-term incentive program with a PSU component tied to hitting a trailing 4 quarter EPS target. This PSU grant would last over a 6.5 year performance period starting September 2018 and ending March 2025.

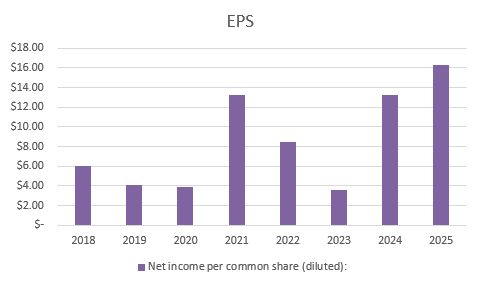

At the time, the trailing 4Q diluted EPS was ~$5.6 on 9.2m diluted shares outstanding. As of the March 2025 10-K, shares outstanding had been reduced to 5.5m, so ~40% of the shares had been repurchased.

Fast forward to EOY2024. The trailing 4Q EPS was ~$14.3. The firm would need to grow EPS by 14% to hit the first hurdle.

Did they hit it? Well, no but also yes. On April 29, 2025, with shares trading around $135, the firm announced Q4 results with this incredible note at the beginning:

During its fourth fiscal quarter, World Acceptance Corporation achieved improved earnings driven by an increase in our tax preparation revenue.

The quarter also benefited from a partial forfeiture of our performance-based restricted shares granted in 2018 that had a $16.35 earnings per share (EPS) performance target (the $16.35 Performance Shares). The forfeiture of such shares resulted in a $2.8 million after tax release of share based compensation expense, resulting in EPS of $16.36 per diluted share on a rolling four-quarter basis. Prior to the forfeiture of such shares, EPS would have been approximately $15.98 for the rolling four quarters.

The March 2025 10-K offers more detail:

During the second quarter of fiscal 2025, it was determined that the $20.45 Performance Shares performance target was no longer probable of being achieved and that the $20.45 Performance Shares would likely be forfeited as of the last day of the performance period in accordance with their terms. As a result and in accordance with ASC 718, the Company reversed $18.5 million in previously recognized stock-based compensation related to the $20.45 Performance Shares during the second quarter of fiscal 2025.

On March 31, 2025, 28% of the unvested $16.35 Performance Shares, or 34,415 shares, were forfeited, which resulted in a $3.5 million release of previously recognized stock-based compensation expense, resulting in EPS of $16.36 per diluted share on a rolling four-quarter basis. Following the forfeiture, the performance target associated with the remaining 72% of the $16.35 Performance Shares, or 88,497 shares, was achieved, and such shares vested on April 25, 2025 after certification of performance achievement by the Compensation Committee.

Wait, what?

That’s right, this isn’t the first quarter where they were able to take advantage of this one little trick your shareholders don’t want you to know. In FY25Q2, they added ~$3.3 to GAAP EPS by forfeiting the $20 strike PSUs, leaving the diluted EPS that quarter at $3.99. Of course, this also plays into the trailing 4Q EPS hurdle. If they hadn’t done this within the designated time frame, the hurdle would not have been able to be met at all.

So basically, the strategy to hit EPS hurdles are:

Set unrealistic EPS target based on trailing 4Qs

Take the operating expense charge in the first few quarters

Buy back shares like mad

Juice earnings by reversing the unrealistic charges during the proper time frame

Profit

This incentive also makes the relentless push to repurchase shares make that much more sense!

WRLD is trading at ~$157, so with a total of 88,497 shares vested, this little maneuver made the management team a collective ~$14M. Not bad for playing accounting games.

Brief Fundamental Overview

Let’s cut to the chase: WRLD is a modern-day usury business. The business operates through >1000 branches and offers loans ranging anywhere from $150 to $25,000 with very high APR (50% blended, with most of the book >36%). Branches can operate with a minimum of two employees. Demographics are surprisingly imbalanced, with 85% of them female. Loans account for 80%+ of overall revenues, and all of the other lines of businesses, from tax preparation to insurance, exist to support this core franchise.

The business targets individuals with sub-prime credit scores, limited savings, and poor credit histories. As one might imagine, the business is highly regulated.

7 year CAGRs:

Interest and Fee Income: .9%

Total Revenue: 1.7%

Net Income: 7.6%

EPS: 15.4%

Shares outstanding: -6.7%

That’s a very brief overview, but it’s clear that the fundamentals haven’t really changed all that much in these past years, outside of the share repurchases, which ultimately impact EPS more than any other metric.

That said, on a go-forward basis, regulatory unwinding may prove to be a tailwind:

One example from the 2025 10-K:

the CFPB has the power to order individual nonbank financial institutions to submit to supervision where the CFPB has reasonable cause to determine that the institution is engaged in “conduct that poses risks to consumers” under 12 USC 5514(a)(1)(C).

In 2022, the CFPB announced that it has begun using this “dormant authority” to examine nonbank entities and the CFPB is attempting to expand the number of nonbank entities it currently supervises. Specifically, the CFPB issued a public designation order setting forth its determination that the Company had met the legal requirements for supervision (the "Order"). Pursuant to the terms of the Order, the CFPB had supervisory authority over the Company until such time as the Order is terminated.

Importantly, on May 12, 2025, the CFPB withdrew the Order, indicating that the CFPB "is shifting its supervisory priorities to focus on pressing threats to consumers" and that supervision of the Company "is not consistent with these priorities." Additionally, the CFPB has recently signaled that, under current leadership, it would take a less aggressive posture with respect to supervision and enforcement of regulated entities.

Another example of this in the footnotes1.

What’s Next?

On June 10, 2025, the compensation committee issued another long-term grant structured similarly to the 2018 grant.

There were some key differences:

Keep reading with a 7-day free trial

Subscribe to Tarot Capital to keep reading this post and get 7 days of free access to the full post archives.