Beat up Adtech Company

This is one of the more asymetric ideas I've found

First: This is going to be a paywalled idea. I don’t think it’s worth sharing, given the quality of the idea. I’ll likely unlock the post after a meaningful amount of time, say ~6 months. Thanks for supporting me, everyone.

Today I’m talking about AppLovin APP 0.00%↑, and why I think it’s one of the most interesting stocks I follow. The thesis is simple, but it starts with a strong governance signal. Adam Foroughi and Vasily Shikin, the CEO and CTO of AppLovin, got a very hefty PSU with some eye-opening price hurdles.

The head of the compensation committee is Edward Oberwager, who is currently a managing director at KKR. We have seen aggressive grants from Private Equity before, and this compensation package is meant to be the only compensation package for the next four years. This is the 4-year price target from the board.

I started to dig into the company immediately with this in mind, and I liked what I found on closer inspection. There are many levers for AppLovin to pull. Here’s the simplified thesis:

IDFA lap begins right now; April 2023 is the 1st anniversary of IDFA.

Many assume IDFA has made APP a worse business; I want to argue that Meditation has increased its relative competitive advantage. Mediation companies are receiving the most information in an ATT, and their market has become a duopoly, and they are the leader.

AppLovin is a tale of two businesses, the ad tech software business, and the mobile apps game. The first is 40% of revenue and ~70% of EBITDA; the second is 60% of revenue and 30% of EBITDA. The software business is meaningfully undervalued and obscured by Mobile Games.1

The market believes the IronSource acquisition is real competition to AppLovin; closer analysis shows that IronSource is misexecuting and Unity is not the juggernaut the market believes it is.

AppLovin will launch its machine-learning-enabled Axon 2 this year; the last time they introduced Axon 1, they took a massive share. This situation could happen again.

They are free cash flow positive, trade for ~7x EBITDA, and likely could grow double-digit revenues on the other side of IDFA. On a DCF, it’s fairly valued at a ~25% discount rate. I think shares could easily double or more in the next year, as investors take note.

I want to next talk about AppLovin and what they do before I talk about the positive investment attributes.

AppLovin bootstrapped its Adtech Stack with its Mobile Games.

AppLovin differs from other “hypergrowth” tech companies as they were initially bootstrapped and profitable. The decision not to take on external capital has shaped the company’s trajectory. Adam Foroughi, the founder, described himself more as “private equity than venture capital.” in his business breakdown podcast. The amazing acquisition strategy proves it. The Business Breakdown podcast on AppLovin is a must-listen.2

AppLovin wanted to be the ad tech standard for mobile games by building an in-game social graph to create better profiles of users. The problem was they had to convince others to share data with them and then convince mobile game makers they could help monetize their games better. That problem was like creating the chicken before the egg.

So they went about the problem backward; they became one of the biggest mobile game companies to test and scale their product, scaled their data product to prove its effectiveness, and convinced others to adopt their solution.

Surprisingly, it worked. They managed to have enough data from their ads to create a network of ads to sell to other mobile games and create custom user profiles. They also started selling ads from their in-house platform called AppDiscovery, helping their mobile games and other mobile game developers grow users. AppLovin became a closed-loop mobile gaming solution.

AppLovin crucially solved both problems for mobile game developers and created both the supply-side solution (MAX) and buy-side solution (AppDiscovery). They bootstrapped this on a portfolio of games that they purchased themselves.

AppLovin today is a business that has finally reached the promised scale, but shares are down 85% from the frothy valuations it IPO’d at. It also went public during the unsustainable growth in mobile games of COVID (more screen time from home), and now it’s one of the most misunderstood stories in public markets. It’s still down 85% from the peak despite its positive 60% YTD run.

The PSUs made me pay attention, and after a closer look, there’s clear value here. There is a sum-of-the-parts story. AppLovin’s improving competitive dynamics, high-quality ad tech business3 hiding within a mobile games conglomerate, and cheap valuation makes it a compelling stock from here. Let’s discuss what AppLovin’s business segments do.

AppLovin Business Overview

Below is the graphic they use to describe their core products, technologies, and App business.

For a company that was mostly a mobile game in 2021, it’s interesting how they highlight the businesses. The Apps business is possibly for sale, given they have created their social graph already, and AppLovin believes they could run their ad tech company without their App network. Let’s discuss the size of each of the businesses.

The software business has become a much larger part of AppLovin in recent years and has a much higher EBITDA margin (65-70%) than the margins of the mobile games business (mid-teens). They are now a software company first. What’s more, the vast majority of EBITDA is derived from the faster-growing business.

The future of this business is Software, while the past is mobile games. As such, I’ll be focusing on the software business in this write-up.

They have three big products and a recently acquired fourth business called Wurl. Wurl is a call option on CTV, but given the size, it could be an important acquisition for AppLovin.

AppDiscovery: User Acquisition for Mobile Game Developers

AppDiscovery is AppLovin's user acquisition and growth platform that focuses on helping mobile game developers, and publishers connect with their target audiences. AppDiscovery enables developers to grow their user base, increase engagement, and drive higher revenue. Effectively AppDiscovery is a mobile games-focused DSP (demand side platform).

Devs go to AppDiscovery to purchase users and impressions when trying to grow their games. AppDiscovery is a demand-side product that is one of the bigger growth funnels for smaller game publishers. Because of the social graph at AppLovin, a game developer can acquire customers with a certain playstyle or likelihood to convert.

Axon resides in AppDiscovery. Axon is their machine learning tool that leverages AppLovin’s social graph and analytics to give much better leads for developers. This means AppLovin can predict users’ interactions non-gaming demand-side platforms cannot. For example, you can acquire a user with an LTV of, say, 2 dollars and will pay back 50% of that in the first 30 days of installation. You can only auction on those players because of AppLovin’s unique social graph. Axon helps predict conversion.

Notable here is that many of the AppDiscovery impressions will be AppLovin games themselves because AppLovin also has a large network of in-game advertisements with their mobile game network. AppDiscovery is a key player in this space, and Axon helped them take share. More on that later.

MAX: Helping Developers Monetize with Advertisements

MAX is AppLovin's in-app bidding and monetization platform to maximize revenue for mobile game developers and publishers. For many game developers launching their first game, the primary way to monetize is through advertisements; MAX is a mediation platform that enables that. MAX is integrated into games via an SDK or code added to the mobile games.

MAX is like an SSP, or supply-side platform, that takes its ad slot inventory and sells the slot to the open market. The big deal with MAX is that they are using real-time bidding (RTB), while IronSource is much newer to RTB. That means each time an advertisement goes up, a live auction happens between all the demand side networks. Mediation is essential for app developers, and IronSource and MAX are in this market. This improves yield and revenue for gaming publishers.

One of the big advantages is that MAX seems to have embraced RTB sooner, and additionally that Google has prioritized AppLovin over Ironsource on their ad spending networking. Here’s a tegus call on the dynamic.

The big players, Facebook, when they first started in their vetting process to bid externally, they went through a really thorough vetting process to make sure that the networks are holding a fair auction and that there was no bias in it. My guess is that they found something within ironSource's system that said to them, all right, we're going to prioritize MAX and we'll come back to ironSource because they're just not there yet. It's probably going to come soon. I mean, they've never been into it. It's probably just a couple of months out, maybe a new year Q1 initiative.

Being late to this kind of thing is important and is how market share is won or lost in the long run. Today IronSource still doesn’t have bidding for Google. I expect AppLovin to be the leader in the in-app advertising segment on a go-forward basis.

After ATT, the ecosystem shifted heavily to Google, and the lack of Admob is a big deal for IronSource.

MAX was an acquisition, which shows AppLovin’s acquisition chops. They acquired the business in 2017. Adjust, and Wurl are also acquisitions.

Adjust: How to Measure Your Ads

Adjust is AppLovin's mobile measurement platform; this was a business acquired in 2021. It’s hard to say why to Adjust is “good,” but it is another part of the platform that led to AppLovin’s dominance. The UI and measurement helped AppLovin create a solution that was more than the sum of its parts, such as feeding its Axon platform. It likely helped augment AppDiscovery’s analytics and tracking data.

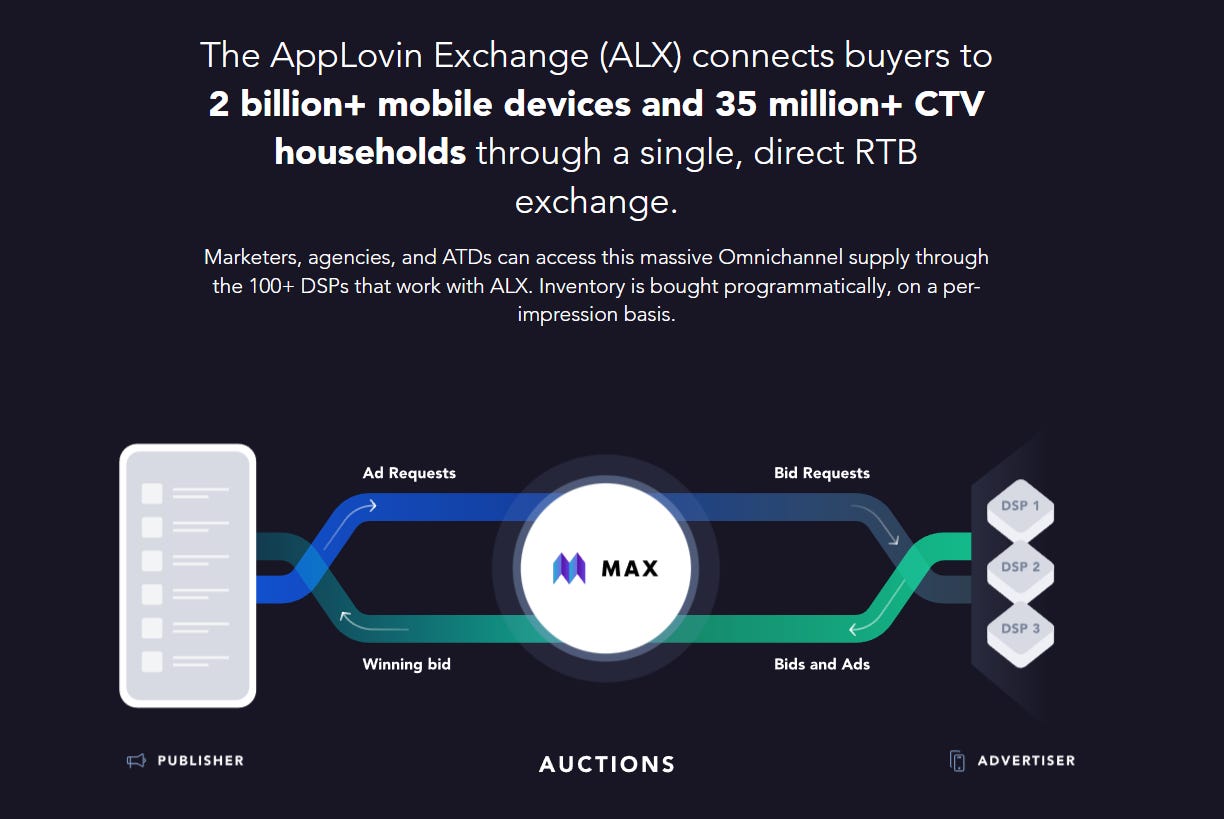

Wurl / AppLovin Exchange: CTV to End-to-End Platform

Wurl is AppLovin's connected TV (CTV) and over-the-top (OTT) advertising platform and is a clear opportunity for AppLovin. Wurl was an acquisition to position itself in CTV better and is an SSP for ad inventory for CTV. Wurl also seems to integrate into their new MAX auction product, which they call ALX.

Put differently, Wurl is probably the new on-ramp for ad inventory for CTV products for mobile games, which don’t have much presence in streaming TV ads.

Wurl, in my view, is one of the biggest opportunities but is a relatively modest business today in AppLovin’s product. This is how Adam described it on the most recent call:

So the same way in mobile, we're an SSP and a DSP. Wurl, today, has a very well-performing SSP business. We, AppLovin, our biggest business is our DSP. We'll couple those pieces and have a full stack offering for Connected TV partners.

Wurl is creating a full stack opportunity for AppLovin for Mobile games looking to monetize on CTV. Now let’s talk about the non-software parts of the business.

Mobile Games: Hyper Casual Conglomerate

AppLovin was mostly known for its hypercasual games, but they’ve begun winding down these businesses. This legacy portfolio is being run for cashflow—they aren’t investing into the growth of the business. That means that despite revenue contraction, EBITDA has exploded.

The mobile games part of the story was important because they were needed to bootstrap the software business, but now it has reached scale, so AppLovin is moving away from that business.

It was a nice coincidence that mobile games exploded during COVID, as screen time and excess income ballooned.

We are starting to see the end of that wave and revenue has gone down. Still, EBITDA has increased. They’ve used this money to reinvest in the core software business. That said, I think the games business suffers from a massive undervaluation within the broader AppLovin structure. I’ll discuss that more in the SOTP analysis portion. Anyway, just understand that while the hypercasual gaming end-market is slowing down, I expect it to continue growing at a very low single-digit revenue on a go-forward basis.

Mediation: The Next Battle

I want to spend a moment here to talk about Mediation, which refers to APP’s in-house ad network optimizer (though it’s also a broader industry term). Read this explainer article if you read nothing else in this write-up. In the pre-IDFA/ATT world, DSPs were the nexus of power, as they had the data, spending, and customer relationship.

Post IDFA, DSPs have much fewer data than they previously had, and interestingly enough, the SSP has more information since they see auction-level data. The SSP sells each ad slot to a collection of bids, which effectively is the “price” or value of the customer. That means the SSPs are the only ones with the full picture. The below graphic from Mobile Dev Memo puts it well.

SSPs are now the ones with the most data. In this space for mobile games, there are only two players, IronSource and AppLovin. AppLovin is the leader with ~60% share, while IronSource is the laggard that has been merged into Unity.

What’s more, AppLovin also has a DSP called AppDiscovery. The specific relationship with mobile games creates a weird relationship not found in other parts of the ad tech stack, as AppLovin is often both the buy and sell side platforms for mobile games. AppLovin has a data advantage not afforded them before, strengthening their relative position.

Now the sellside (SSP) has more information into these bids than the sell side, but if they offer a full stack ad exchange (see ALX above), then what can happen is AppLovin has a full data advantage that we haven’t seen before.

The “why now” of the aggressive PSUs grants is likely understanding this relationship and anticipation of the new Axon product launch. Put differently, the market is pricing their business as if permanently impaired, and I believe their relative position just strengthened. And now they are locked in a battle for a duopoly with Unity and Ironsource. Let’s talk about them now.

Competition Overview

The other big names, IronSource and Unity, merged last year, closing the deal in November. Unity bought Ironsource, which was a worse-run version of AppLovin. However, Unity is the mobile game engine of choice, so they have a much higher funnel relationship with developers than AppLovin.

AppLovin tried to buy Unity (bold move Adam) but failed as Unity decided to buy IronSource instead and spurned the AppLovin deal. They were similar-sized enterprise values when this happened (50B+ range!)

Since then, high multiple businesses have derated, and shares are down 80%+. But these businesses are not broken and have now consolidated into a Duopoly. This type of consolidation is good for the survivors (remember TTD as the last DSP among 10s?). Unity and AppLovin are the last two ships in the harbor; let’s discuss their competitive strengths.

Unity and Ironsource vs. AppLovin

I’m going to start with Unity. Unity is one of the strongest game engines in the world, with Epic’s Unreal Engine as a second-place competitor. Here’s a chart of the cumulative games on the Steam store.

That’s all time, but in 2022 that number is even higher. Unity is the clear leader, with Unreal in second place.4

Despite the game engine’s prominence, their primary monetization method is advertisements! However, Unity was always known more for its engine than its advertisement expertise, so it bought IronSource.

IronSource, in many ways, was the perfect acquisition. Now Unity Devs have IronSource added to their games without any additional integration, which creates even better lock-in at the top of the funnel. The strategic sense of the acquisition was great, but the optics were not. There was a bit of controversy as they laid off people and bought IronSource just days later. Read the thread.

In particular, the timing of shutting down their internal game effort to dogfood the Unity engine and instead bought IronSource. Devs felt their complaints about the engine improvements were not being heard, and the Unity CEO had an interview that effectively called all Devs not making money “fucking idiots.”

Ferrari and some of the other high-end car manufacturers still use clay and carving knives. It’s a very small portion of the gaming industry that works that way, and some of these people are my favourite people in the world to fight with – they’re the most beautiful and pure, brilliant people. They’re also some of the biggest fucking idiots.

Some context is that the CEO of Unity is John Riccitiello, the former CEO of EA when they were voted the “Worst Company in America.” People hate him, and calling developers who often consider themselves artists “fucking idiots” is a bit of a PR nightmare. He even had to do a public apology tweet in July of 2022.

While IronSource is likely a great asset for Unity, the PR nightmare, execution issues (not integrating IronSource into Google), and other problems likely plague Unity. What I’m trying to get at is that the Unity + IronSource deal is good, but AppLovin has been gaining market share the entire time, even with the overall market growing 50%+.

What’s more, AppLovin started with a much smaller share and has been growing a larger part of that pie. The revenue here is likely not completely comparable, but I know they have 60%+ revenue within the broader mediation space. One of the big incremental growth drivers was Axon launching. You can see it in their numbers as they took ~15%+ share.

Another big market share gain was when they bought MoPub. They acquired the customers of the underinvested MoPub from Twitter and then migrated the entire customer base to AppLovin in five months. Meanwhile, IronSource is still not verified on Google! AppLovin is an execution machine. They acquired MAX, and now it’s a material part of their business. They move fast and win often.

AppLovin, in my opinion, does not get the appreciation it deserves, given it’s at a worse position in the ad tech stack, but its execution is no slouch. Ultimately, it looks like the industry will settle into a duopoly. The lean execution focused AppLovin and the land and expansion of Unity. Both companies likely will continue to take share from smaller players that will be slowly weeded out of the system.

But I still like AppLovin’s stock much more. Part of it is price. The other is embedded call options and a history of execution. Let’s discuss the call options before moving on to valuation.

AppLovin’s Call Options

The big call option is the launch of Axon 2. As you see in the table above, when they launched Axon, revenue accelerated, and they took tons of market share from IronSource and Unity.

Since the launch of our machine learning engine, AXON, our software platform revenue growth has accelerated for 3 consecutive quarters. And during the second quarter, our software platform revenue more than tripled year-over-year. -Q2 2021 AppLovin Earnings

This matters because they are launching Axon 2, which will be launched in 2023. If history repeats itself, revenue will accelerate for a few quarters.

Well, now we're working on AXON 2. We're going to use some of these new technologies for release some point in 2023. We believe this new platform and upgrade to our core technology will make an immense impact on our business and for our business partners. -Q4 2022 AppLovin Earnings

Another opportunity is Wurl, which creates a new opportunity in CTV, one of the fastest-growing buckets in ad spending. The acquisition of customers and a new pipeline of mobile game customers are likely interesting and incremental. The above SSP and DSP combo for games sounds compelling.

Lastly, the sale of mobile games is among the biggest catalysts for the stock. Adam has said the business could be for sale, and given the very public comps, I think the RemainCo could be very cheap.

The games business is worth over a billion, or ~.8x sales or 5x EBITDA. That would mean RemainCo is trading for ~7x EBITDA, still a discount to every public pure-play ad tech company despite having best-in-class metrics. IronSource, the smaller and less profitable business (half the EBITDA margin), got bought out for ~20x EBITDA! AppLovin is way too cheap! Here’s a basic SOTP below.

These are all levers that Adam can pull and were part of the calculus when Adam and the compensation board decided to do the PSUs. Adam isn’t a slouch, and execution is their strong suit. They have levers to pull, and each of them could quickly change the story for the company, thus making the PSU price hurdles possible.

Valuation and Conclusion

I hope by now that I made the point that Axon could reaccelerate growth and that numbers will improve as software becomes a larger part of the pie. But to me, the real margin of safety here is the price. This is a very cheap stock.

Let’s say the business didn’t have the mobile game business; it would be ~7x EBITDA, with a 65% EBITDA margin and the ability to grow at a 20%+ revenue rate. That seems massively mispriced to me.

What’s more, is that APP is the single cheapest stock on an EV/EBITDA basis compared to its peers. PLTK is a pure-play mobile game company, not even ad tech! You can argue that APP deserves to trade at a premium to MGNI, APPS, and PLTK while at a discount to TTD and U. Below is a price chart over time. APP’s multiple has gone from hero to zero, once trading at a premium to MGNI, APPS, and PLTK, and now trading at a discount.

This is on a sales basis. As a friendly reminder, these are the EV/Sales, and APP is trading closer to the APPS and PLTK peers than MGNI, TTD, and U.

Considering the standalone software business, it’s the highest EBITDA margin of these publicly listed companies. Here are the listed comps. Software is doing ~65% EBITDA margin currently.

The take rate here is not SSP-like but rather closer to DSPs. This is not a single-digit take rate, but rather 20%+. It’s hard to differentiate because MAX says they will take 10 to 25 cents per dollar and prioritize gross dollars over everything.

Lastly, I want to do some modeling and analysis of forward numbers. First, this is a classic mix-shift story. The market does not appreciate that they are a software-first business now, and the revenue growth will accelerate as the faster-growing business is a larger portion of revenue.

In the future, most of the EBITDA will be from Software, yet they are not receiving these multiples. This is the opportunity. It will grow faster with a mix shift; it will be more profitable with a mix shift.

I also took a stab at modeling the company. I believe that Sell-Side has the company model extremely conservatively for the annual because APP only guides one quarter in advance. For AppLovin to be at consensus, it implies either a sharper deceleration of mobile games (possible) or Software to stop growing completely (unlikely).

My numbers are higher than consensus in the out years, but this is primarily based on software revenue differences. I believe that Software can sustain its growth of 20%+ revenue from Axon, Wurl, or further consolidation in the industry. Meanwhile, I am much more bearish on mobile games, assuming a sluggish ~3% revenue growth in the out years.

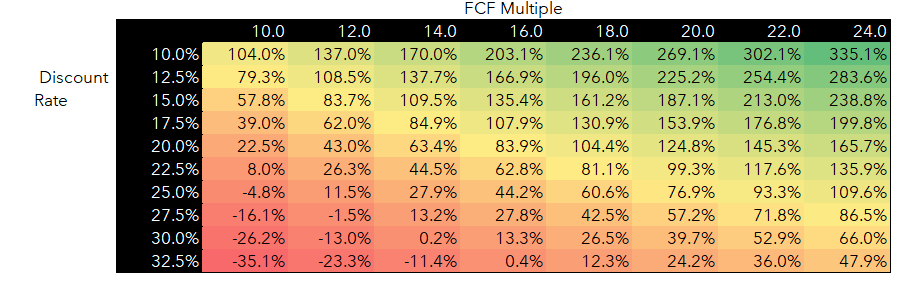

That brings me to the DCF. We can underwrite a very impressive price by assuming low FCF conversion (~50-60%), low-teens revenue growth, and improving margins from the increasing shift to software.

Using these assumptions, we can get to some pretty hefty hypothetical returns. There is a 100% upside assuming a ~10% discount rate and a 10x exit FCF multiple. At a ~10x exit multiple, it’s a 22% discount rate for “fair value.” That’s an absurd and massively underpriced business if even some of the execution comes through.

Even if my estimates are a bit too aggressive, the price can more than make up for it. Here are some of the key characteristics of the business:

Part of a mobile gaming duopoly

Has multiple levers to pull (Axon, Wurl, Mobile Games sale)

Has an aggressive founder who is highly incentivized with a large grant

Post-COVID hangover left-for-dead stock trading at objectively cheap levels while still growing EBITDA at a healthy rate

Very modest multiples with aggressive discount rates justifying a price much higher today on a DCF with a 10% (very academic) WACC!

Investing isn’t perfect, but it’s hard to get a better setup than that.

Risk Section

The biggest risk I can think of is that mobile games and the software business get separated, and the performance of software implodes because of it. Software prioritizes the data and metrics they control most, likely their own games. The belief is that the two businesses are truly apart, but what if they cannot be split up? That would ruin the SOTP pitch.

The next big risk to this thesis is that ad tech is a terrifying industry with lots of change. IDFA ruined everything and frankly, it could be upended again by one of the big players. That’s a risk you’ll have to take, but there’s already a lot of room for error at this price. In terms of specifics, the biggest risk in this arena is if Google applies similar ATT regulations as Apple, further nuking profitability.

Another risk is that dilution and messy FCF conversion make this less clean than we’d like. For example, Wurl has some goofy vesting schedules that could dilute the minority shareholder.

Importantly, post-closing, we're also planning to create a multiyear performance-based incentives plan for Sean and his team that very much closely aligns with our shared success. The plan contains minimum and maximum annual revenue and EBITDA thresholds for the years 2023 through 2025. The amount earned in a particular year ranges from 0 at the minimum to a specific amount at the maximum per year and will be paid in equity. For example, in the final year of the agreement, if in 2025 revenue is less than $200 million, that year's performance bonus would be 0. If revenue is greater than $550 million and the EBITDA threshold is also met, that year's annual bonus paid in equity would be $330 million. If every year's performance bonus in '23, '24 and '25 is maxed out, the total payment will be $600 million in equity. We're excited that this aligns very much with our shared success.

That would be half of the economic value accrued to shareholders going directly back to Wurl founders! Nutty grants, but it’s also clear that the management team understands and likes incentives in PSUs. If this happens, Wurl is likely a huge player, and the improvement in the business would likely offset some of the dilution. Still, it’s something to think about. The economy could mess this up. It partially already has, and if the brunt of the economic recession is ahead of us, I think that there could be more pain ahead. But that being said, we are in the depths of the IDFA lap, and things should start to lap next quarter. That’s a reason to be hopeful.

There are some real risks here, but I’m greatly reassured by the fact that management is so tightly aligned with price hurdles. So, I like the shares.

Industry Overview (Addendum)

Mobile Games have Two Ecosystems, In-App Purchases, In-App advertisements. The advertisements often serve as the top funnel for games offering In-App purchases.

Below is a chart of the breakout of users. DAU is up 8%, according to Unity, but paying users are down 2% from 2021. Advertising is up against this backdrop.

There’s been a shift of preference to ads and IAP over subscriptions.

Meanwhile, there’s been a big shift towards ad revenue in 2022 compared to 2021.

Interestingly retention in games is improved by ads!

The entire mobile ecosystem suffers from economic headwinds, but DAUs are still up YoY, which bodes well. Mobile gaming is not dead. For more information, I would refer to this really helpful state of games by Unity.

Further, hyper-casual games seemed to have bottomed in Q4 of last year.

Fun fact this is my favorite setup. Investors often underappreciate the mix shift, as most look only one year in advance. Understanding what three years of margin shifts does to a business is powerful.

Sidenote, I love the business breakdowns curse. Stock is about 80% since that podcast, which might have marked the top. Time to pick up the breakdown.

I’m aware of how much of an oxymoron this is.

https://www.reddit.com/r/dataisbeautiful/comments/10vcj5e/oc_game_engines_market_shares_on_steam_all_time/