Will it Blend?

Betting on Lower or Stable Rates

Blend (BLND) is a $900 million market-cap software company specializing in digitizing the borrowing process, primarily within mortgage and housing-related consumer lending. Its technology enables partner banks and credit unions to integrate customizable solutions within their existing origination infrastructure by outsourcing to Blend.

The company debuted in the public markets as part of the infamous 2021 IPO class, initially trading as high as $21 per share before bottoming out near $0.50 in May 2023. Following significant cost-cutting measures and a turnaround in fundamentals, Blend's stock has rebounded to approximately $3.50. The company now stands on the verge of profitability, benefiting from operational leverage and favorable macroeconomic trends, such as stabilizing/declining interest rates. The stock's movements are closely tied to data on HELOCs, refinancing, and new home sales.

Business Overview

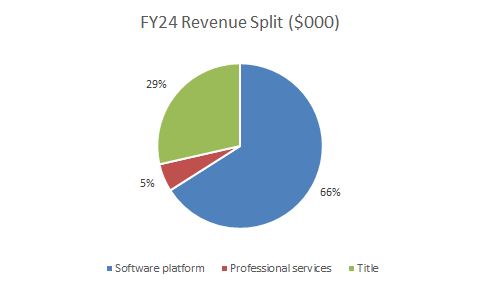

The firm operates through two segments: Blend Platform and Title.

Blend Platform (Software)

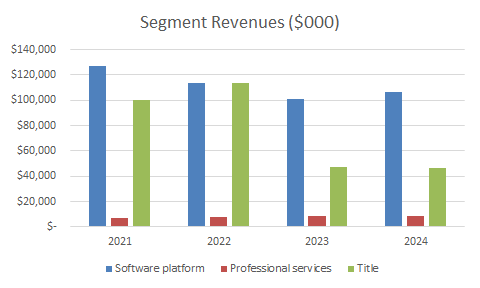

The Blend Platform segment offers origination software and professional services, supporting the processing of nearly $1.2 trillion in loan applications in 2024. The company follows a "land and expand" strategy, beginning with a limited product offering before broadening its services within existing client relationships. Revenues are predominantly consumption/transaction-based, though some fixed-fee components exist.

While mortgage-related services remain the dominant revenue driver, consumer banking has been the primary growth engine in recent quarters, growing over 40% in FY24. The mortgage suite segment has demonstrated positive year-over-year (YoY) growth for the past two quarters, indicating fundamental improvement. Both segments are driven by housing activity.

Blend's gross margins remain robust at approximately 70%, in line with SaaS peers.

Title

In June 2021, Blend acquired 90% of Title365, a title insurance agency, to help transaction completion for customers. Gross margins for this segment range between 10% and 15%. It’s not a particularly big driver of value and only makes up 8% of gross profits.

Market Share and Customer Base

Blend primarily serves banks and financial institutions that lack the resources or interest to develop and maintain their own technology infrastructure. Management occasionally discloses a new logo win and the firm seems to have good traction among top 100 and even top 30 banks or lenders in any given vertical. While mega-banks are unlikely to adopt Blend at scale, the company has demonstrated strong traction among large, mid-sized, and small banks across the U.S.

Once these relationships are established and Blend manages the technology stack, it becomes steadily more difficult to offboard. The capabilities become vestigial and the capital investment necessary to replicate becomes too high a hurdle.

In its 24Q3 earnings report, Blend disclosed that it facilitated approximately 20% of all mortgage originations in 2023.

Fundamental Drivers

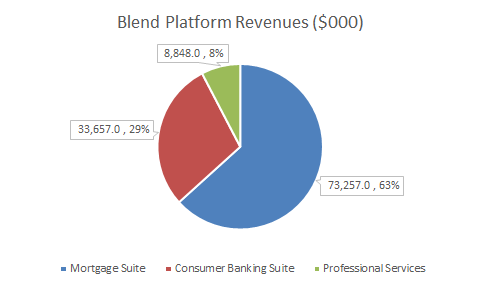

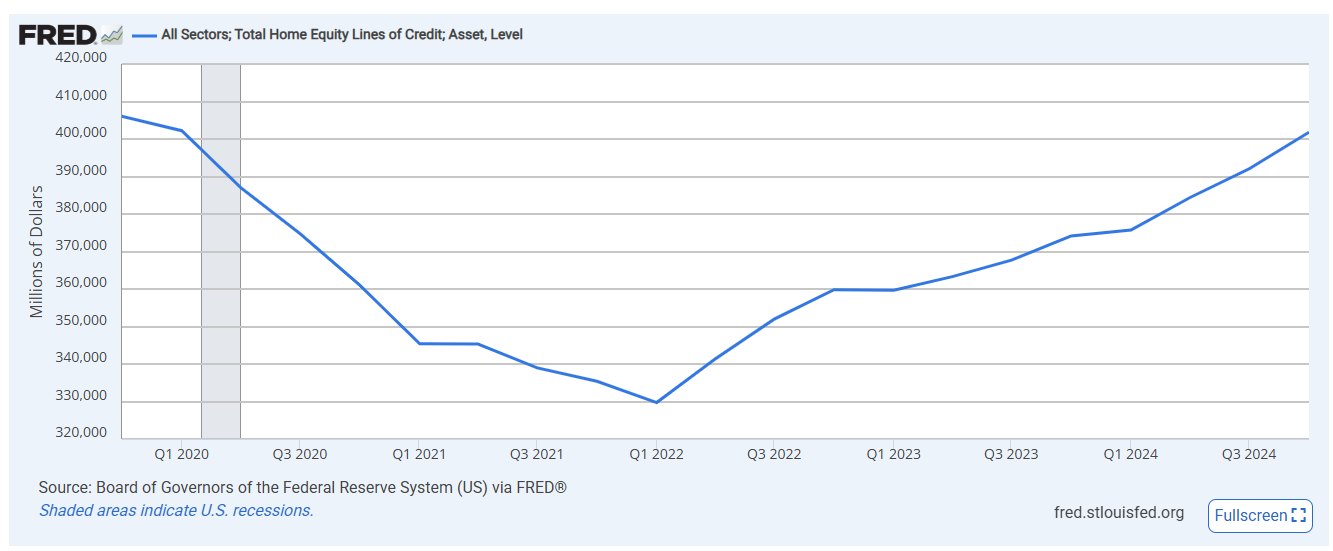

Initially focused on mortgage origination through Mortgage Suite, Blend has since prioritized Consumer Banking given the strong uptake and volumes there. While still linked to residential financing, Consumer Banking extends beyond traditional mortgage origination, covering areas such as HELOCs and refinancing.

Management has projected a 40% compound annual growth rate (CAGR) for consumer banking revenue from FY23 to FY26. This implies that Blend’s Consumer Banking revenue could approach the scale of its mortgage segment in the near future.

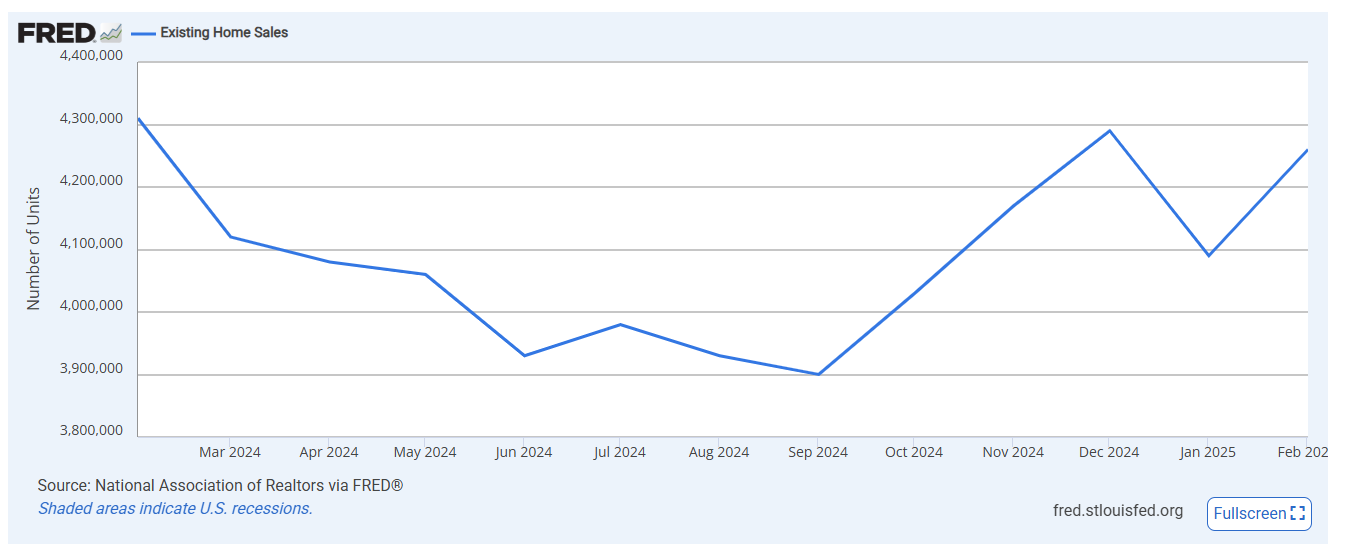

The 24Q4 earnings call highlighted a 50% YoY increase in Blend’s sales pipeline, largely driven by mortgage activity recovery.

And we mentioned this in the prepared remarks, but we're up sort of 50% year-over-year in our pipeline. And I think a lot of that is due to the strength of the mortgage pipeline coming back.

Additionally, the company has launched two new products focused on refinancing and HELOCs, which have already begun generating revenue.

I think we said we have 3 customers live on the Rapid refi products and one on the Rapid home equity product. And the Rapid home equity product, the results are stark in the comparison between the Rapid solution and our flagship solution, which is one they've had live for years.

And so we're already generating revenue from the Rapid product. It's still early, though. It takes time to, as you know, sell, implement, get these customers live and ramped up. But throughout the year, you should see that start to ramp up with the Rapid products.

Home equity in particular is an effective tool for customers:

Early results are showing 1.5x pull-through advantage and decreasing application of funding cycle times by at least 20% as well as enhancing utilization of Home Equity lines by consumers for debt consolidation.

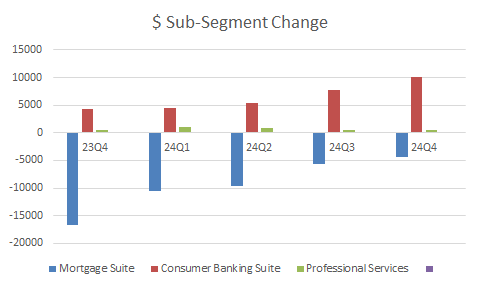

In fact, home equity-related transactions appear to be a particularly big driver of the consumer banking unit, per the FY24 10-K:

Consumer Banking Suite revenue increased $10.0 million, or 42%, primarily due to an increase in home equity transactions and incremental platform fees, an increase in attach rates of our digital closing solution, higher volume of deposit account openings, offset by lower consumer lending transactions with our customers.

The deployment of these new products should prove to be a massive tailwind once (if?) rates come down.

Trend Drivers

Interest Rate Trends: Stable or declining interest rates benefit Blend, while rate hikes pose challenges.

HELOC & Refinancing Growth: Strong demand in these areas is driving consumer banking expansion.

Mortgage Origination Recovery: The core business declines have stabilized and reversed, with the two latest quarters experiencing MSD YoY growth. It’s still a large revenue driver, so if the regular origination business starts to accelerate, there will be a greater inflection in fundamentals. Investors are fairly well aware of this, which is why shares move on NARI data releases regarding home sales.

Primary Risks

Macro: If rates start going up again, bad things happen.

Customer Concentration: Per the 2024 10-K, the top five customers in the Blend Platform segment were ~33.0% of segment revenues. There are 23 customers in the Blend Platform segment generating more than $1 million in annual revenue, which represented 62.8% of FY24 segment revenues.

Cash Burn: Assuming FY24 net income of -$43m is an accurate approximation of the cash burn, the firm only has ~2 years left of cash and marketable securities to go through before having to raise more capital. That said, the actual cash situation is better than optically looks, given that a good chunk of that is stock-based compensation. It’s not a huge issue for now, but something to keep an eye on if the macro drivers don’t come through.

Valuation

Blend currently trades at an 8.3x revenue multiple on the Blend Platform segment. Given a base-case scenario where mortgage revenue remains flat and consumer banking continues its 40% growth trajectory, projected revenue growth for FY25 and FY26 would be 11.6% and 14.6%, respectively. Applying a conservative 10x multiple to FY26 Blend Platform revenues suggests ~50% upside in the stock price. If interest rates decline, revenue growth could accelerate further, supporting a higher valuation.

In fact, the management implied price target for FY26 is much higher.

Management’s Bet/The Edge

Keep reading with a 7-day free trial

Subscribe to Tarot Capital to keep reading this post and get 7 days of free access to the full post archives.