WDAY Dodges a Bullet

After Getting Hit by 47 Cruise Missiles

This is a joint post between myself and UnlearningCFA , a very sharp governance analyst. Check ‘em out!

Imagine you buy a nice bulletproof house in a good neighborhood for a million bucks. Things are great for a while, but then, suddenly someone starts shooting at your house. Now, everything’s holding up fine so far (on account of it being bulletproof), but after the millionth bullet, you start to doubt how bulletproof it will be after the next million bullets. As time goes on, the shooter also appears to be improving significantly.

What do you think the fair value of the house is? Well, maybe not zero, but probably south of a million bucks.

Welcome to the SaaSpocalypse!

There is literal carnage going on in SaaS-land. Terminal values are being destroyed left & right, with investors selling first and asking questions later.

Whether you think SaaS is completely doomed or going to the moon, one trend that has started to gain some momentum is making personnel changes to lead companies through this period of significant change. Recent examples include: Salesforce, Oracle, UiPath, Klaviyo, and many more.

On February 6th, Workday WDAY 0.00%↑, a $30bn mkt cap human resources software business, joined the deck-chair reshuffling by replacing its CEO with Aneel Bhursi, its executive chair and co-founder. Aneel’s time at Workday is summarized as follows:

Co-Chief Executive Officer from August 2020 through January 2024

His transition to executive chair from co-CEO had been telegraphed in a press release from December 2022.

Chief Executive Officer from 2014 to August 2020

Co-Chief Executive Officer from 2009 to 2014

President from 2007 to 2009

Co-founded Workday in 2005.

Fast forward to today, with Aneel describing his return as CEO:

We’re now entering one of the most pivotal moments in our history. AI is a bigger transformation than SaaS — and it will define the next generation of market leaders. I’m energized to return as CEO, working alongside our presidents Gerrit Kazmaier and Rob Enslin, and I’m excited about the opportunity in front of us.

While the announcement and timing is intriguing, the compensation structure is what we were curious about:

$1.25MM salary

200% bonus opportunity

$60MM in RSUs vesting over four years

$75MM in PSUs

Five year performance period with various tranches based on stock price targets (not yet disclosed).

Not eligible for additional equity awards until 2027

The press release notes that the grant date for both the RSUs and PSUs is March 5th. With Workday set to announce FY 2026 results after the close on February 24th, I can’t help but think that he may want to kitchen sink guidance a bit, so that his awards can be priced off of a lower base.

While the dollar amount of Aneel’s award is significant on an absolute basis, it’s important to remember that it’s still smaller than the ~8.5MM shares he currently owns worth ~$1.1B. It’s also worth noting that the stock voting agreement with his cofounder represents ~70% of voting power.

It’s safe to say that Aneel (age 59) could’ve rode off into the sunset with his billion and left this difficult transition for someone else to figure out. However with founders, sometimes these business transitions feel deeply personal. As a writer that typically focuses on incentive compensation, one needs to realize that billionaires typically desire something even more important than money: long-term reputation.

It’s also probably quite personal for Aneel because Peoplesoft (his former employer) was the victim of a hostile takeover by Oracle in 2004 during the wreckage of the dot-com bust. There is almost certainly a shark out there waiting to harvest Workday for the free-cash-flow and he most likely wants to prevent that.

Since the start of 2026, Workday is down ~30% due largely to AI fears. The stock is back to price levels not seen since the bottom of the 2022 bear market and the depths of the COVID crash.

Key questions include: Will power accrue to the agents completing tasks in the B2B software, instead of the software itself? Are systems of record businesses better insulated than others? Will revenue continue to be priced on a per-seat basis, or will it be based on outcomes generated for customers?

Time will tell whether the doomers or the bagholders are right.

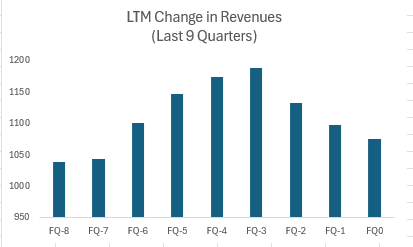

As for the business itself, it continues to sport a 97% gross revenue retention, which is both world-class, and demonstrates the intense stickiness of the product. That said, revenue growth has been decelerating for the past 4 quarters.

At today’s stock price, Workday trades at ~3x EV/NTM Revenues, which is the cheapest it’s been in a very long time. With its ~75% gross margin and ~9% EBIT margin, one could imagine costs could be optimized if there was true intent (Sales & Marketing expense is ~27% of revenue).

The general consensus among tech investors today is that Workday R&D productivity is the lowest they’ve seen of any tech company, ever. So there’s likely a ton of visceral fat to trim there as well.

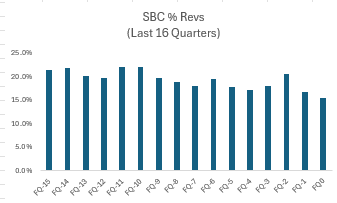

It is also worth noting that share-based compensation (SBC) as a percentage of revenue, gross profit, and adjusted EBIT has been falling for the past 4 years.

Employees have cheered on Aneel’s return, specifically calling out the reduction in SBC as a negative. The historical compensation structure for the entire SaaS space relies on heavy SBC and price appreciation to bail them out. Returning to that would not be positive for the stock!

While some are rightly skeptical of the willingness of SaaS companies to optimize their margins, we note that their ability to do so has been more than proven-out.

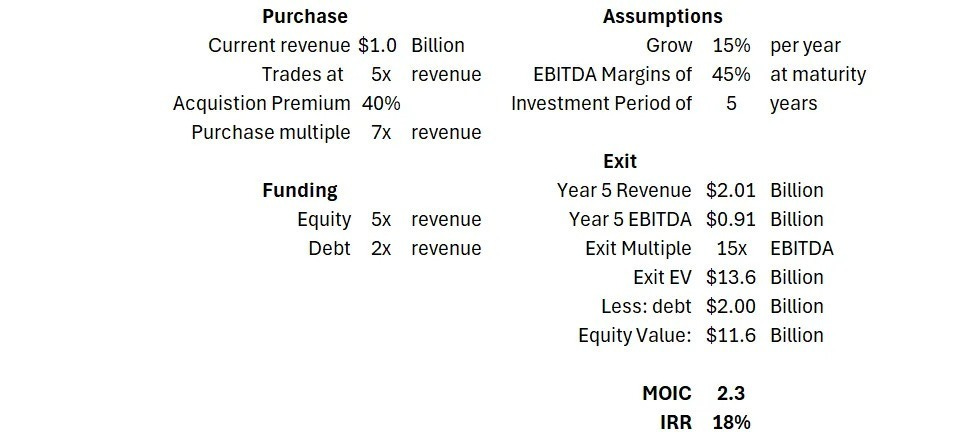

In October 2025, we got a sneak peek into how the biggest private SaaS investor, Thoma Bravo, thinks about their buyout model. On the All-in podcast, Orlando Bravo alluded to 45% normalized EBITDA margins for SAAS companies that they’ve bought. Here is a basic outline of the model described in the podcast:

Multiples have changed a lot…

At the end of the day, SaaS is currently a falling knife drenched in the blood of those with more courage than us. Whether the multiple compression reflects future business prospects or not remains to be seen.

We know that Aneel has tremendous amounts of reputational and financial risk on the line, but will that be enough?

| A guest post by

|