Quick Note: Insurance Brokers Exposed to Medicare Advantage

Taking Shelter in Healthcare

Quick Notes are brief thoughts I think are worth sharing. I think they’ll likely be situations where it’s difficult to get clarity on the actual business dynamics, but there’s a lot of torque built in. So, if you do take a position, size small.

On April 7th, 2025, CMS set the Medicare Advantage rate increase to 5.06% for 2026. This is very good for every insurer, but especially good for highly exposed insurers like Humana (HUM 0.00%↑) and CVS (CVS 0.00%↑).

In the CY 2026 MA and Part D Advance Notice, CMS proposed updates to payment factors for CY 2026 and received a wide variety of comments on our proposals. CMS appreciates the submitted comments. We considered applicable comments as we finalized the policies contained in the CY 2026 Rate Announcement. The final policies in the CY 2026 Rate Announcement are projected to result in an increase of 5.06%, or over $25 billion, in MA payments to plans in CY 2026.

It’s also great for SLQT 0.00%↑, a $500m market-cap DTC insurance broker that serves as a middleman between consumers and insurers. The broker doesn’t generate revenues directly from consumers, but takes commissions from the insurers based on the value of the plan premiums.

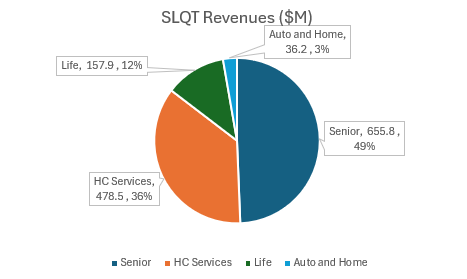

We represent approximately 25 leading, nationally-recognized insurance carrier partners, including carriers owned by UnitedHealthcare (“UHC”), Humana, Wellcare, and Aetna. MA and MS plans accounted for 91% of our approved Senior policies for the year ended June 30, 2024, with other ancillary type policies accounting for the remainder.

The thesis is pretty simple: it’s going to be more lucrative for health insurers to get folks signed up for Medicare Advantage → they’re going to pump out advertisements → Medicare Advantage sign-ups at the brokers increase.

Thus, the firm should disproportionately benefit from the increase in MA spending.

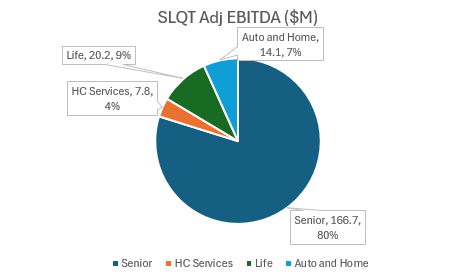

The Senior segment has healthy margins (FY24 25% adj EBITDA), but it’s quite volatile depending on market conditions.

I view this as a trade, and not an investment, especially given how boom and bust the brokerage business is. It’s not a particularly high quality company, so the idea is that you ride it through a quarter or two, then get out before the cycle turn—easier said than done, of course.

The stock is also interesting from the governance angle in a way that makes this more actionable:

Management Compensation Upside

Keep reading with a 7-day free trial

Subscribe to Tarot Capital to keep reading this post and get 7 days of free access to the full post archives.