Part and Parcel

The Greek Goddess of The Hearth Takes Over the Board

It’s uncommon for a board member of a publicly traded corporation to loudly resign due to disagreements related to a company’s corporate governance practices.

Jill Sutton’s strongly worded letter to the board of Pitney Bowes (NYSE:PBI) in October of 2024 tells a gripping story: Kurt Wolf, through his hedge fund Hestia Capital, has taken over the board of PBI and installed their preferred CEO, demoting Jill from Board Chair in the process.

This recent episode is part of an activist campaign that began in late 2022, which led to Hestia successfully securing four out of five nominated board seats in 2023.

While Sutton raises valid concerns about governance, we believe Hestia’s heavy handed approach presents potential opportunities for shareholders.

Author’s note: Readers, if you’re already familiar with PBI, please scroll down to ‘The Edge’ section, which highlights the key unusual characteristics of this idea.

Company Overview

Pitney Bowes Inc (PBI) is an integral part of the nationwide parcel transportation network, operating parcel sorting centers and selling associated equipment through its ~10,500 employees. As the largest workshare partner of the USPS, the company processed over 15 billion pieces of mail in 2023. Given the seasonality of shipping demand, a larger portion of revenue is generated in Q4 compared to other quarters. Overall, PBI operates in a very competitive and secularly declining space. Optimistic!

PBI operates through three key segments:

SendTech: Primarily generates revenue through mail support services, including subscriptions for mailing and shipping equipment, as well as financing solutions. The segment maintains strong margins but operates in a shrinking market. It also has a bank subsidiary.

A close partner. Presort Services: The largest workshare partner of the USPS, handling over 15 billion pieces of mail annually. The business benefits from outsourcing efficiencies but faces industry-wide volume declines.

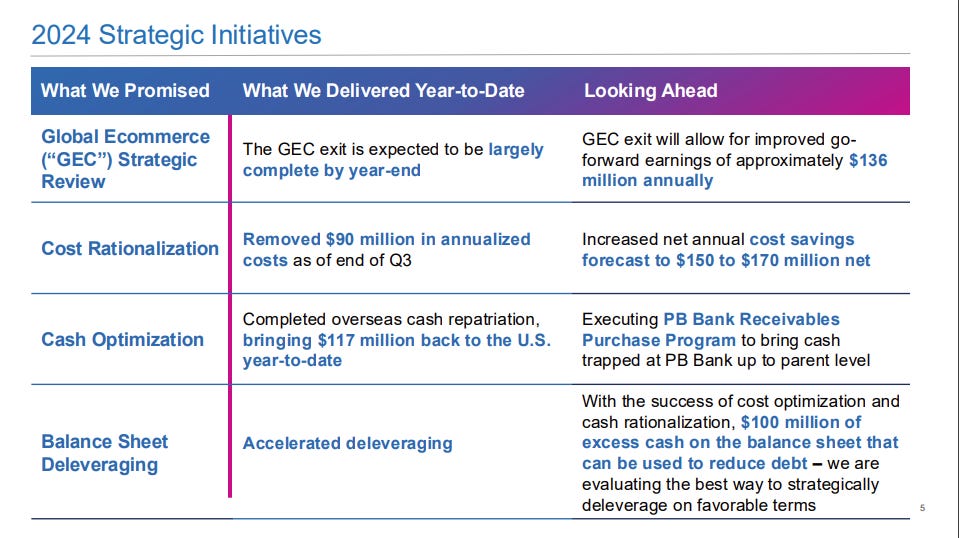

Global E-Commerce (GEC): This segment has been a financial burden and is undergoing liquidation. Parts of it are being sold to stem losses. This should save the broader business some $130m a year.

The following data is from the 2023 10-K, published in Feb 2024:

Both of the remaining segments are tied to physical mail, which has been declining in relevance for nearly two decades.

SendTech revenues primarily come from support services, e.g. subscriptions for equipment and shipping solutions, operationalized primarily through maintenance contracts. Basically, the segment provides equipment and services to make mailing easier for businesses and individuals. There’s even a bank attached to the segment that helps clients with finance or lease equipment.

It’s the global leader in mailing (an eroding market).

PreSort is the largest work share partner of the USPS and helps process 16 billion+ pieces of mail a year. They are the number #1 in mail sortation, which is a complex and time intensive task that clients are more than happy to outsource. I’m going to assume that you, the reader, are familiar with the nitty gritty of complex systems—in this case, speedily and accurately delivering a piece of mail to the right person, at scale—and have faith that there are dozens of small annoyances that can be outsourced to the right partner (in this case, PBI).

Hestia’s Activist Strategy

Hestia first disclosed their PBI ownership stake in November of 2022, ahead of 2023 Board nominations. In January of 2023, they distributed an activist deck declaring their intent to nominate seven candidates to the eleven person board.

While we were not privy to the discussions between Hestia and large shareholders, we presume that the bulk of the meetings involved significant time loudly emphasizing the above price chart.

The activist deck targeted management and specifically called out the board chairman Michael Roth and CEO Marc Lautenbach for being responsible during the extended period of fundamental decline.

In March of 2023, having seen the writing on the wall, chairman Michael Roth and two other directors announced their retirement at the end of the yearly board cycle. Coincident to this, the existing directors decided to reduce the size of the board to nine people, effective at the annual meeting. In response, Hestia shrunk their nomination slate to five candidates.

Ultimately, four Hestia nominees made it onto the board in May of 2023, including Hestia founder Kurt Wolf. The one Hestia nominee that didn’t make it onto the board was Lance Rosenzweig, who they also wanted to install as CEO.

By October 2023, CEO Marc Lautenbach stepped down as CEO, making way for interim leadership. In subsequent months, additional changes further consolidated Hestia’s control.

So ended a turbulent 2023.

Key Developments in 2024 and 2025

January 2024: PBI entered into a cooperation agreement with Hestia, limiting the firm’s ownership to 9.9%. The agreement is scheduled for automatic termination 30 days prior to the director nominations for the 2026 annual meeting. Board chair Mary Guilfoile announced her departure alongside the appointment of two new directors (William S. Simon and Jill Sutton).

March 2024: newly appointed director William Simon announced his departure from the board, to be replaced with… Lance Rosenzweig, the only director that wasn’t voted in during Hestia’s initial campaign.

April 2024: Board restructuring continued, culminating in Hestia’s full takeover. The board would be reduced to five members. As it so happens, the original company-nominated directors from the 2023 slate all made it onto the board.

At the end of the month, Lakeview, a 2.55% holder of PBI shares, issued an open investor letter demanding that the GEC unit be sold and asking for stability after high turnover amongst management and in the boardroom.May 2024: Interim CEO Jason Dies was replaced by Lance Rosenzweig as interim CEO. PBI hosted a special call on May 29th, 2024 to discuss the transition. CEO Rosenzweig emphasized cost savings and shareholder alignment through an equity-heavy compensation package (>97% equity).

July 2024: Cost-saving initiatives exceeded expectations, leading to a positive market response. The firm noted that $70m in savings had been achieved in the current quarter and that expectations of total savings had increased from the original $60-$100m to $120m-$160m, realized over the remainder of 2024.

August 2024: GEC filed for Chapter 11 bankruptcy, incurring ~$150 million in costs.

October 2024: Jill Sutton resigned from the board, citing governance concerns. New board appointments followed, along with the installation of Lance Rosenzweig as permanent CEO.

November 2024 - January 2025: Debt repayment efforts continued. Ultimately, $280 million of high-yield notes were paid down with the intention of refinancing further out. The firm has ~$250m left in the bank after the $280m repayment of the highest yielding 2028 notes (~11%, ouch).

Fundamentals, Financials, and Valuation

Despite some green shoots in growth areas and excellent margin expansion during this turnaround, PBI still faces very real headwinds in the core business. The declining legacy segments, particularly SendTech, could pose challenges, especially post-IMI replacement cycle.

However, assuming continued cost optimizations and somewhat stable market conditions, my FY25 projections suggest net income of approximately $190 million and free cash flow at similar levels. With a market cap near $1.5 billion, this implies a forward P/E ratio of around 8.3x—reasonable for a declining business.

Key Assumptions:

FY25 SendTech revenues decline 5% and Presort remains stable vs. FY24 estimates

Margins continue to reflect 2024 cost-saving benefits (32% for SendTech, 23.6% for Presort)

Interest expenses drop by $30 million due to debt repayment (in the absence of knowing the details of the planned refinancing)

variable rate debt highlighted Restructuring costs remain one-time expenses

CapEx and D&A remain in-line with prior years

Sources of Fundamental Upside:

Growth in emerging business areas (e.g., SaaS solutions persist in double digit growth)

Further cost reductions beyond the already realized $120-$160 million

Stabilization or reversal of declines in legacy markets

Risks:

Accelerated decline in end-markets

Harder comps in 2025

USPS political impacts

The Edge

The following combination of the related key factors suggests that Hestia has a plan in mind to achieve significant price appreciation over the next year (give or take a few months):

Keep reading with a 7-day free trial

Subscribe to Tarot Capital to keep reading this post and get 7 days of free access to the full post archives.