BWXT's Nuclear Strategy Approaches Critical Mass

Radiating Confidence (And Free Cash Flow)

BWX Technologies (BWXT 0.00%↑) is $9B market-cap nuclear technology business servicing both US government (80% of sales) and commercial customers (20%). The stock is fairly expensive at a ~30x trailing P/E, which reflects the high-quality nature of the business and the unique position it holds as a government contractor interfacing with highly sensitive nuclear material.

A recent special grant to management was flagged by our process and led to a review of the business to identify fundamental areas where management thinks they may have an advantage against traditional defense names.

Brief Fundamental Overview

The firm is a core supplier to the US government’s nuclear programs, specifically the Navy’s nuclear powered submarines and aircraft carriers.

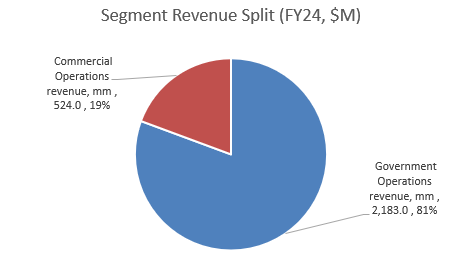

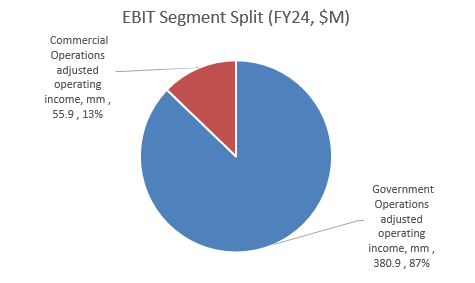

This is a capital intensive long-cycle business driven by long-term US government contracts, which contributed 81% of FY24 revenues and 87% of operating income.

Government Operations

This segment manufactures and sells nuclear components to the US Navy, DoE, and other government organizations, going back as far as the 1950s. It also provides services for nuclear-related maintenance at weapons sites, laboratories, and factories. Last but not least, the segment develops nuclear reactors for a variety of applications, not just for terrestrial power, but for potential propulsion in space. ~80% of segment revenues come from the DOE or the Naval Nuclear Propulsion Program.

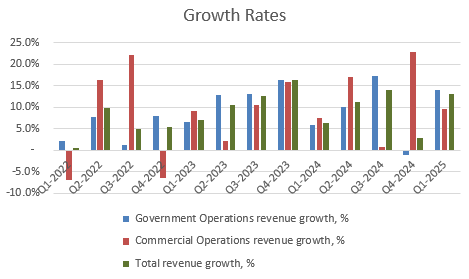

It represents 80% of revenues ($2B) with ~18% operating margins, growing at an 8.2% CAGR from FY21 to FY24. Government contracts are the engine of BWXT’s growth. These are stable long-term contracts, and the strong positioning is liable to lead to future revenue streams as well. Contracts are signed ~2 years in advance and run for 8 years.

The stability and reliability of the business should be immediately obvious given the confidentiality and high-trust requirements for any contractor that engages with anything nuclear related. It’s the only business allowed to handle certain kinds of nuclear-related materials.

Commercial Operations

Commercial Ops has a number of growth areas, but is smaller in overall opportunity size vs. the government business.

Our Commercial Operations segment supplies heavy nuclear components, specialized engineering and maintenance services, nuclear fuel, fuel handling systems and tooling delivery systems for CANDU reactors.

Only 20% of revenues, but growing at a slightly faster 8.8% CAGR over the FY21 to FY24 period. It’s a solid business with high barriers to entry—BWXT is the only commercial heavy nuclear manufacturer on the continent—but in the base case it isn’t going to be driving most of the earnings growth. Consider it a source of optionality. It’s not a bad business, just less relevant.

A lot of the more speculative nuclear tailwinds are concentrated under this segment. For example, BWXT is well positioned as a picks-and-shovels supplier to firms attempting to deploy small modular reactors (SMRs). SMR market size is estimated to grow to $300B by 2040.

There’s also a nuclear medicine subsegment focused on both diagnostics and therapeutics. A lot of the work being done comes from the Nordion acquisition in 2018. The market is estimated to grow to $30B by 2030 and there are 90+ radiopharmaceuticals in the pipeline.

Multiples

Multiples are on the higher end of the historical range.

Metrics and Drivers

Note that backlog and bookings provide solid through to future revenues. In the FY24 10-K, management noted that ~48% of disclosed backlog would be recognized by EOY FY25. This disclosed value has fluctuated over time. For example, in the FY23 10-K, it was ~51%.

CapEx requirements should decline over the next few years because the company invested heavily ahead of critical projects. Management targeting Maintenace Capex at 4% of sales. FCF conversion should go up to management’s targeted 90%.

Management’s Bet

Keep reading with a 7-day free trial

Subscribe to Tarot Capital to keep reading this post and get 7 days of free access to the full post archives.